Binomial Count Estimation with bayesDP

Donnie Musgrove

2026-06-25

Source:vignettes/bdpbinomial-vignette.Rmd

bdpbinomial-vignette.RmdIntroduction

The purpose of this vignette is to introduce the

bdpbinomial function. bdpbinomial is used for

estimating posterior samples from a Binomial event rate outcome for

clinical trials where an informative prior is used. In the parlance of

clinical trials, the informative prior is derived from historical data.

The weight given to the historical data is determined using what we

refer to as a discount function. There are three steps in carrying out

estimation:

Estimation of the historical data weight, denoted , via the discount function

Estimation of the posterior distribution of the current data, conditional on the historical data weighted by

If a two-arm clinical trial, estimation of the posterior treatment effect, i.e., treatment versus control

Throughout this vignette, we use the terms current,

historical, treatment, and

control. These terms are used because the model was

envisioned in the context of clinical trials where historical data may

be present. Because of this terminology, there are 4 potential sources

of data:

Current treatment data: treatment data from a current study

Current control data: control (or other treatment) data from a current study

Historical treatment data: treatment data from a previous study

Historical control data: control (or other treatment) data from a previous study

If only treatment data is input, the function considers the analysis a one-arm trial. If treatment data + control data is input, then it is considered a two-arm trial.

Estimation of the historical data weight

In the first estimation step, the historical data weight is estimated. In the case of a two-arm trial, where both treatment and control data are available, an value is estimated separately for each of the treatment and control arms. Of course, historical treatment or historical control data must be present, otherwise is not estimated for the corresponding arm.

When historical data are available, estimation of is carried out as follows. Let and denote the number of events and sample size of the current data, respectively. Similarly, let and denote the number of events and sample size of the historical data, respectively. Let and denote the rate parameters of a Beta distribution. Then, the posterior distributions of the event rates for current and historical data, under vague (flat) priors are

and

respectively. We next compute the posterior probability . Finally, for a discount function, denoted , is computed as where may be one or more parameters associated with the discount function and scales the weight by a user-input maximum value. More details on the discount functions are given in the discount function section below.

There are several model inputs at this first stage. First, the user

can select the discount function type via the

discount_function input (see below). Next, choosing

fix_alpha=TRUE forces a fixed value of

(at the alpha_max input), as opposed to estimation via the

discount function. In the next modeling stage, a Monte Carlo estimation

approach is used, requiring several samples from the posterior

distributions. Thus, the user can input a sample size greater than or

less than the default value of number_mcmc=10000. Finally,

the Beta rate parameters can be changed from the defaults of

(a0 and b0 inputs).

An alternate Monte Carlo-based estimation scheme of

has been implemented, controlled by the function input

method="mc". Here, instead of treating

as a fixed quantity,

is treated as random. Because

is recomputed at each Monte Carlo draw using a single pair of posterior

samples, the resulting sequence of

values can exhibit noticeable Monte Carlo variability. First,

,

is computed as

where

is the

th

quantile of a standard normal (i.e, the pnorm R function).

Here,

and

are estimates of the variances of

and

,

respectively. Next,

is used to construct

via the discount function. Since the values

and

are computed at each iteration of the Monte Carlo estimation scheme,

is computed at each iteration of the Monte Carlo estimation scheme,

resulting in a distribution of

values.

Discount function

There are currently three discount functions implemented throughout

the bayesDP package. The discount function is specified

using the discount_function input with the following

choices available:

identity(default): Identity.weibull: Weibull cumulative distribution function (CDF);scaledweibull: Scaled Weibull CDF;

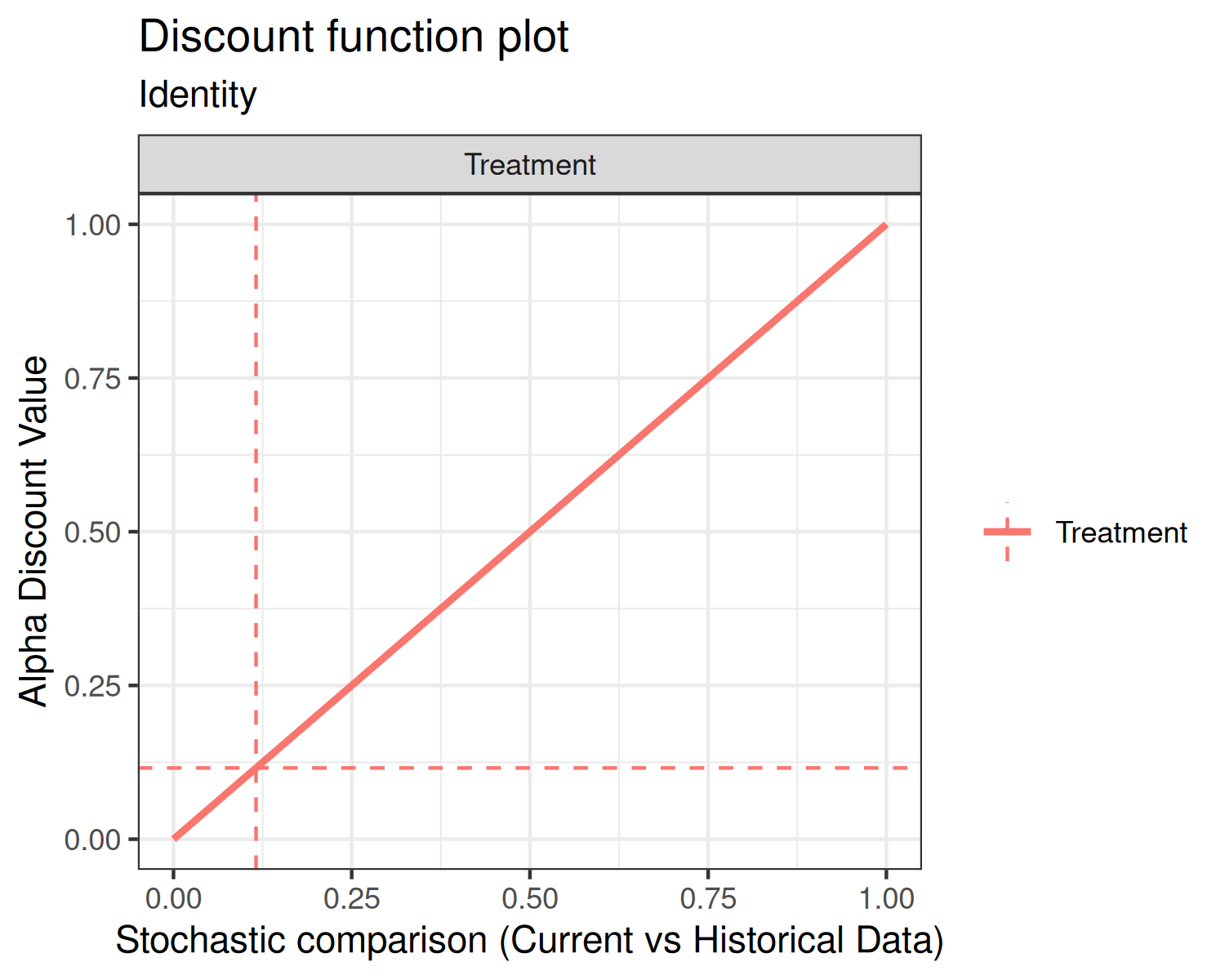

First, the identity discount function (default) sets the discount weight .

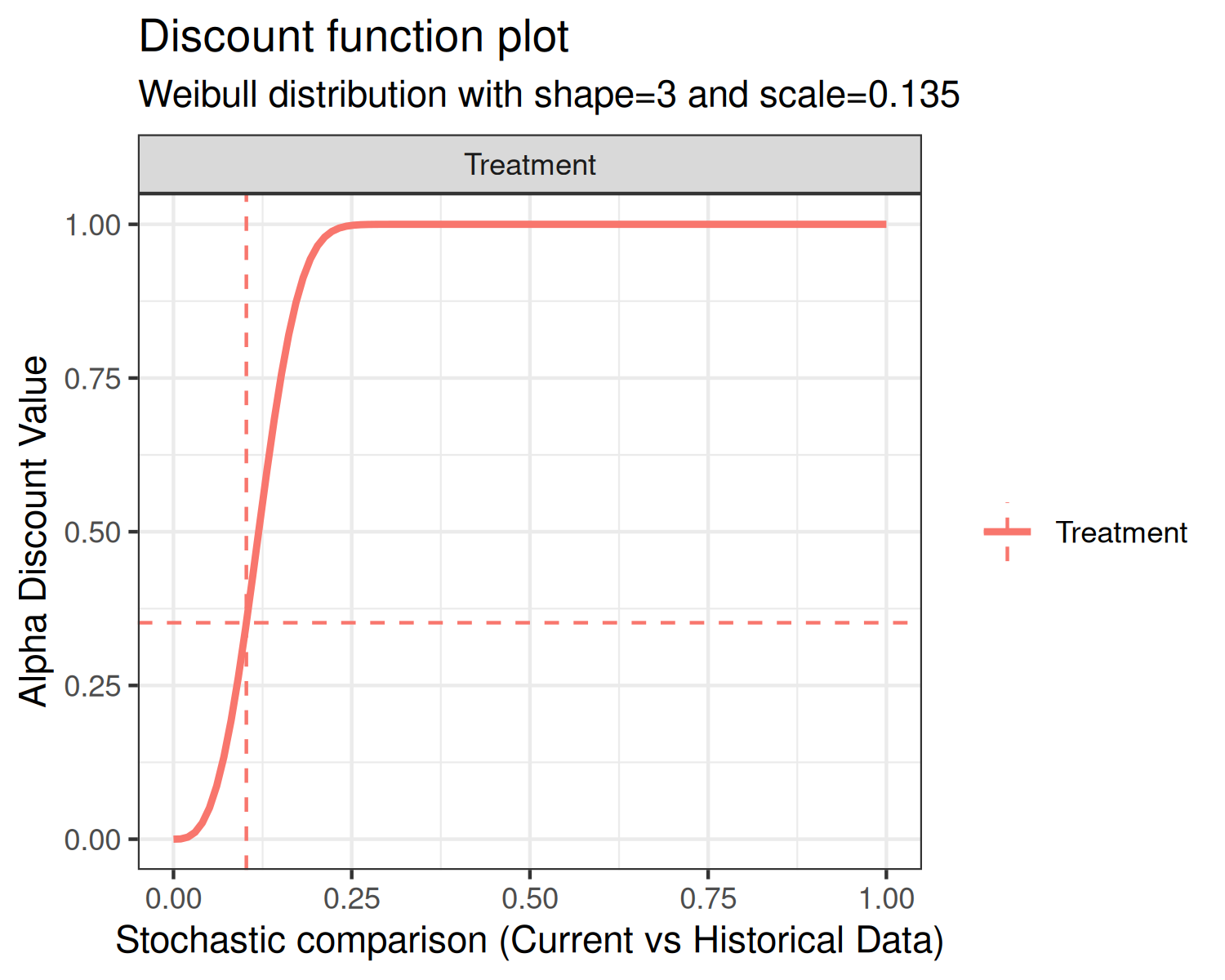

Second, the Weibull CDF has two user-specified parameters associated

with it, the shape and scale. The default shape is 3 and the default

scale is 0.135, each of which are controlled by the function inputs

weibull_shape and weibull_scale, respectively.

The form of the Weibull CDF is

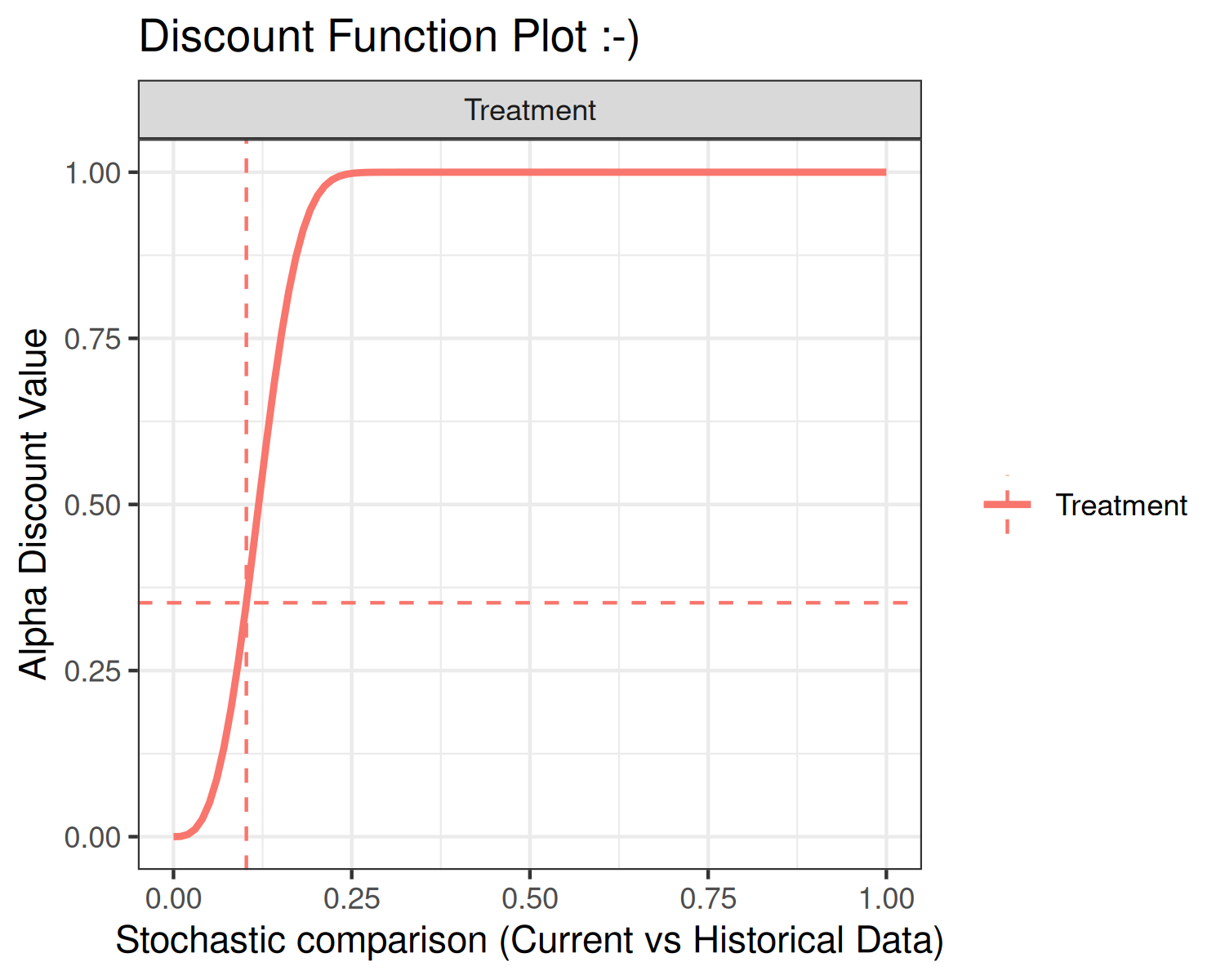

The third discount function option is the Scaled Weibull CDF. The

Scaled Weibull CDF is the Weibull CDF divided by the value of the

Weibull CDF evaluated at 1, i.e.,

Similar to the Weibull CDF, the Scaled Weibull CDF has two

user-specified parameters associated with it, the shape and scale, again

controlled by the function inputs weibull_shape and

weibull_scale, respectively.

Using the default shape and scale inputs, each of the discount

functions are shown below.

In each of the above plots, the x-axis is the stochastic comparison between current and historical data, which we’ve denoted . The y-axis is the discount value that corresponds to a given value of .

An advanced input for the plot function is print. The

default value is print = TRUE, which simply returns the

graphics. Alternately, users can specify print = FALSE,

which returns a ggplot2 object. Below is an example using

the discount function plot:

Estimation of the posterior distribution of the current data, conditional on the historical data

With

in hand, we can now estimate the posterior distribution of the current

data event rate. Using the notation of the previous section, the

posterior distribution is

At this model stage, we have in hand number_mcmc

simulations from the augmented event rate distribution. If there are no

control data, i.e., a one-arm trial, then the modeling stops and we

generate summaries of the posterior distribution of

.

Otherwise, if there are control data, we proceed to a third step and

compute a comparison between treatment and control data.

Estimation of the posterior treatment effect: treatment versus control

This step of the model is carried out on-the-fly using the

summary or print methods. Let

and

denote posterior event rate estimates of the treatment and control arms,

respectively. Currently, the implemented comparison between treatment

and control is the difference, i.e., summary statistics related to the

posterior difference:

.

In a future release, we may consider implementing additional comparison

types.

Inputting Data

The data inputs for bdpbinomial are y_t,

N_t, y0_t, N0_t,

y_c, N_c, y0_c, and

N0_c. The data must be input as (y,

N) pairs. For example, y_t, the number of

events in the current treatment group, must be accompanied by

N_t, the sample size of the current treatment group.

Historical data inputs are not necessary, but using this function would

not be necessary either.

At the minimum, y_t and N_t must be

input. In the case that only y_t and

N_t are input, the analysis is analogous to using

prop.test. Each of the following input combinations are

allowed:

- (

y_t,N_t) - one-arm trial - (

y_t,N_t) + (y0_t,N0_t) - one-arm trial - (

y_t,N_t) + (y_c,N_c) - two-arm trial - (

y_t,N_t) + (y0_c,N0_c) - two-arm trial - (

y_t,N_t) + (y0_t,N0_t) + (y_c,N_c) - two-arm trial - (

y_t,N_t) + (y0_t,N0_t) + (y0_c,N0_c) - two-arm trial - (

y_t,N_t) + (y0_t,N0_t) + (y_c,N_c) + (y0_c,N0_c) - two-arm trial

Examples

One-arm trial

Suppose we have historical data with y0_t=25 events out

of a sample size of N0_t=250 patients. This gives a

historical event rate of 0.1. Now, suppose we have current data with

y_t=15 events out of a sample size of N_t=200

patients, giving an event rate of 0.075. To illustrate the approach,

let’s first give full weight to the historical data. This is

accomplished by setting alpha_max=1 and

fix_alpha=TRUE as follows:

set.seed(42)

fit1 <- bdpbinomial(y_t = 15,

N_t = 200,

y0_t = 25,

N0_t = 250,

alpha_max = 1,

fix_alpha = TRUE,

method = "fixed")

summary(fit1)##

## One-armed bdp binomial

##

## Current treatment data: 15 and 200

## Historical treatment data: 25 and 250

## Stochastic comparison (p_hat) - treatment (current vs. historical data): 0.3664

## Discount function value (alpha) - treatment: 1

## 95 percent CI:

## 0.0663 0.1194

## sample estimates:

## 0.0902Based on the summary output of fit1, we can

see that the value of alpha was held fixed at 1. The

resulting (augmented) event rate was estimated at 0.0902 which is

approximately the event rate if we combined the historical and current

data together, i.e., (15 + 25) / (200 + 250) = 0.089. Note

that the print and summary methods result in

the same output.

Now, let’s relax the constraint on fixing alpha at 1.

We’ll also take this opportunity to describe the output of the plot

method.

set.seed(42)

fit1a <- bdpbinomial(y_t = 15,

N_t = 200,

y0_t = 25,

N0_t = 250,

alpha_max = 1,

fix_alpha = FALSE,

method = "fixed")

summary(fit1a)##

## One-armed bdp binomial

##

## Current treatment data: 15 and 200

## Historical treatment data: 25 and 250

## Stochastic comparison (p_hat) - treatment (current vs. historical data): 0.3664

## Discount function value (alpha) - treatment: 0.3664

## 95 percent CI:

## 0.0566 0.1211

## sample estimates:

## 0.085When alpha is not constrained to one, it is estimated

based on a comparison between the current and historical data. We see

that the stochastic comparison, p_hat, between historical

and control is 0.3664. Here, p_hat is the posterior

probability of the comparison between current and historical data. With

the present example, p_hat = 0.3664 implies that the

current and historical event rates are moderately different. The result

is that the weight given to the historical data is shrunk towards zero.

Thus, the estimate of alpha from the discount function is

0.3664, and the augmented posterior estimate of the event rate moves up

from 0.075 observed in the current data to a value closer to 0.089.

Many of the the values presented in the summary method

are accessible from the fit object. For instance, alpha is

found in fit1a$posterior_treatment$alpha_discount and

p_hat is located at

fit1a$posterior_treatment$p_hat. The

sample estimates and CI are computed at run-time. The

results can be replicated as:

## [1] 0.085

CI95_augmented <- round(quantile(fit1a$posterior_treatment$posterior, prob=c(0.025, 0.975)),4)

CI95_augmented## 2.5% 97.5%

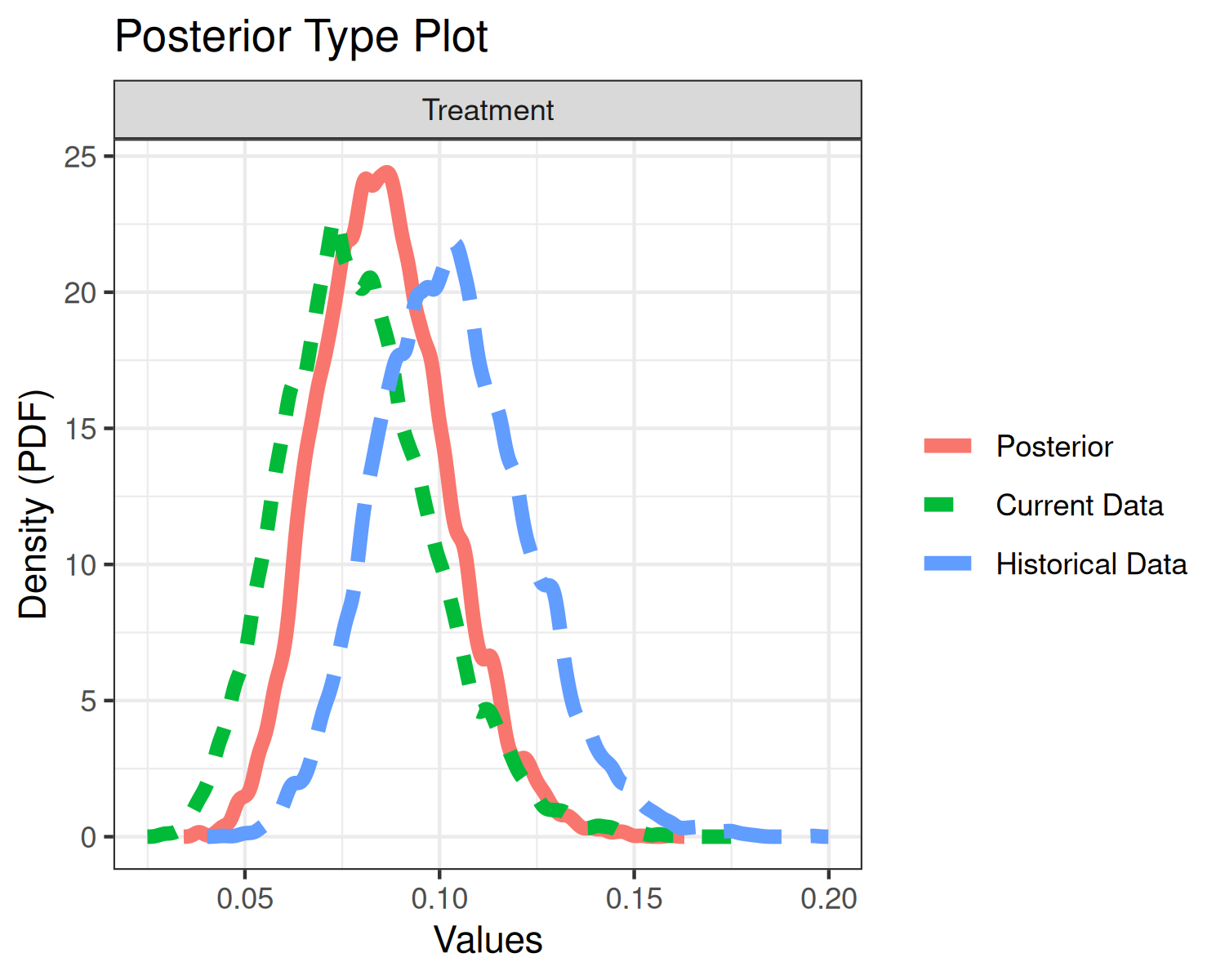

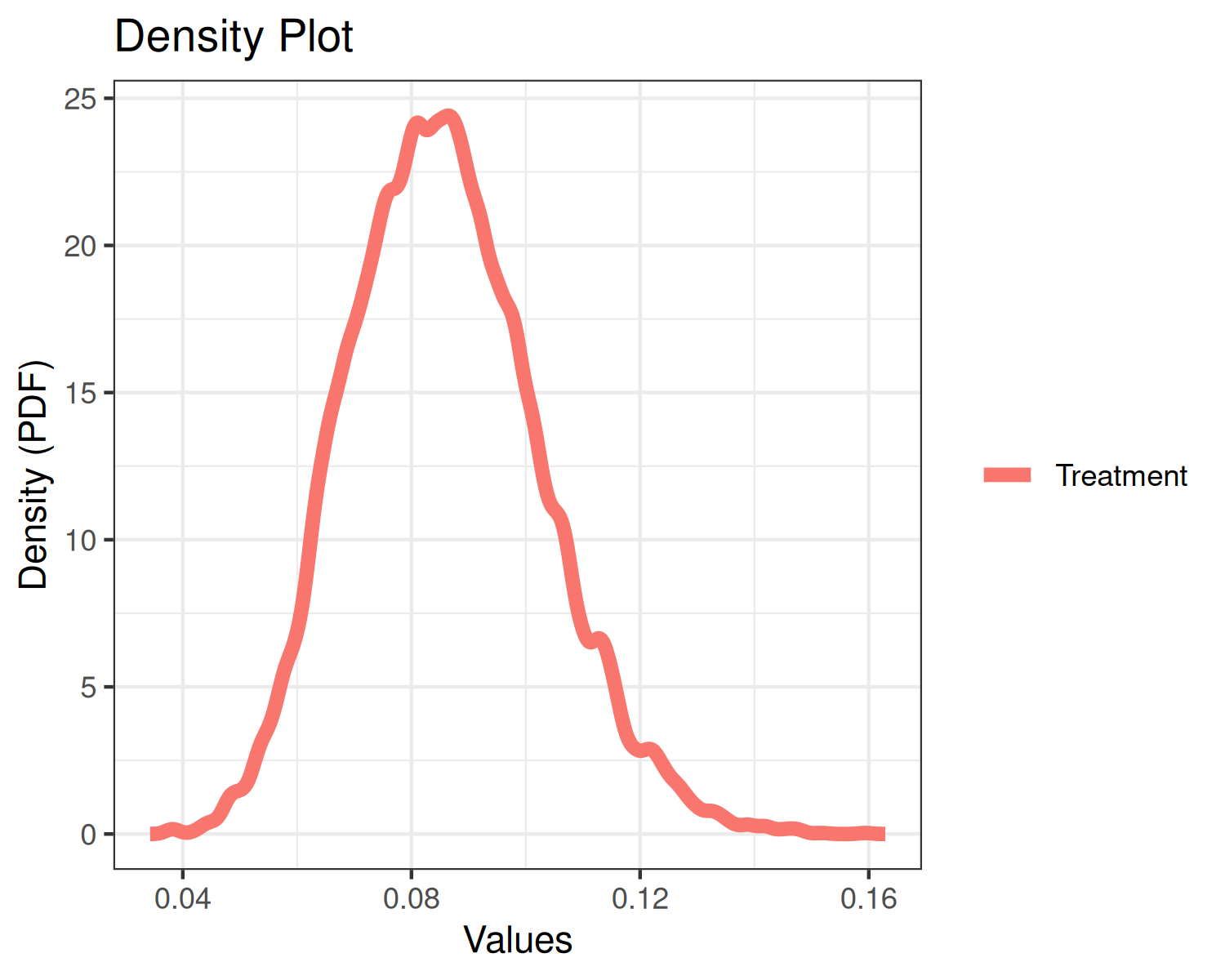

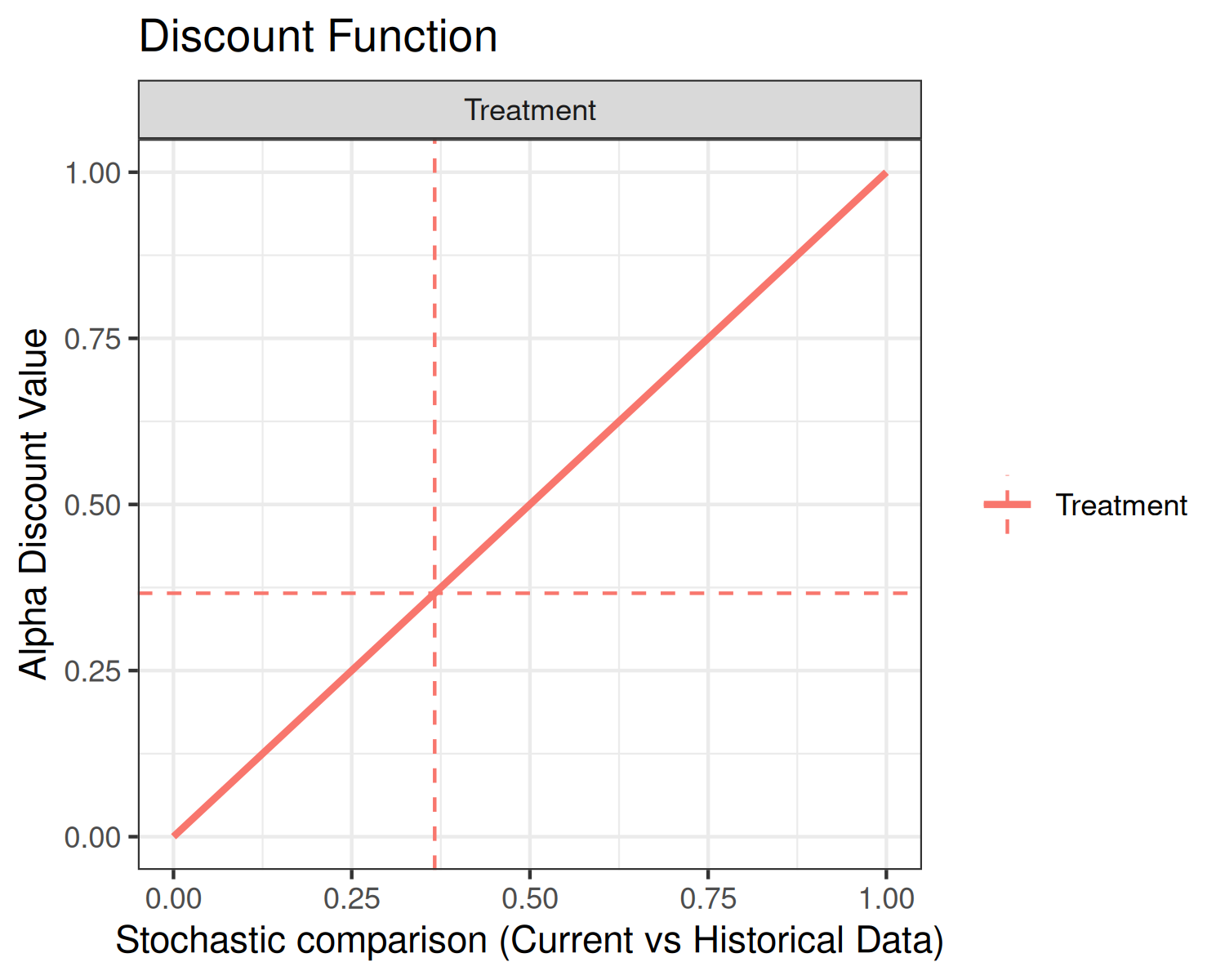

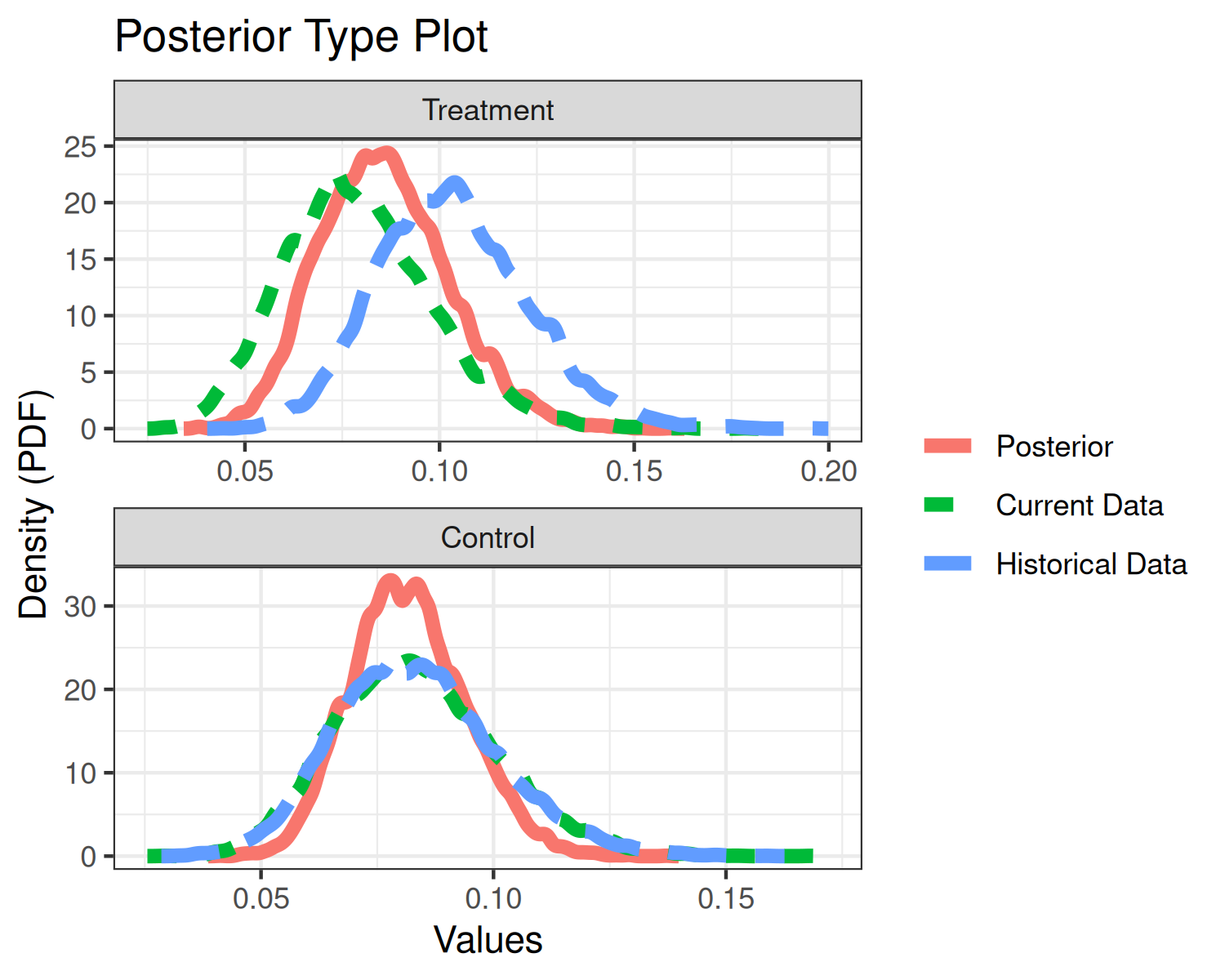

## 0.0566 0.1211Finally, we’ll explore the plot method.

plot(fit1a, type="posteriors")

plot(fit1a, type="density")

plot(fit1a, type="discount")

The top plot displays three density curves. The blue curve is the density of the historical event rate, the green curve is the density of the current event rate, and the red curve is the density of the current event rate augmented by historical data. Since little weight was given to the historical data, the current and posterior event rates essentially overlap.

The middle plot simply re-displays the posterior event rate.

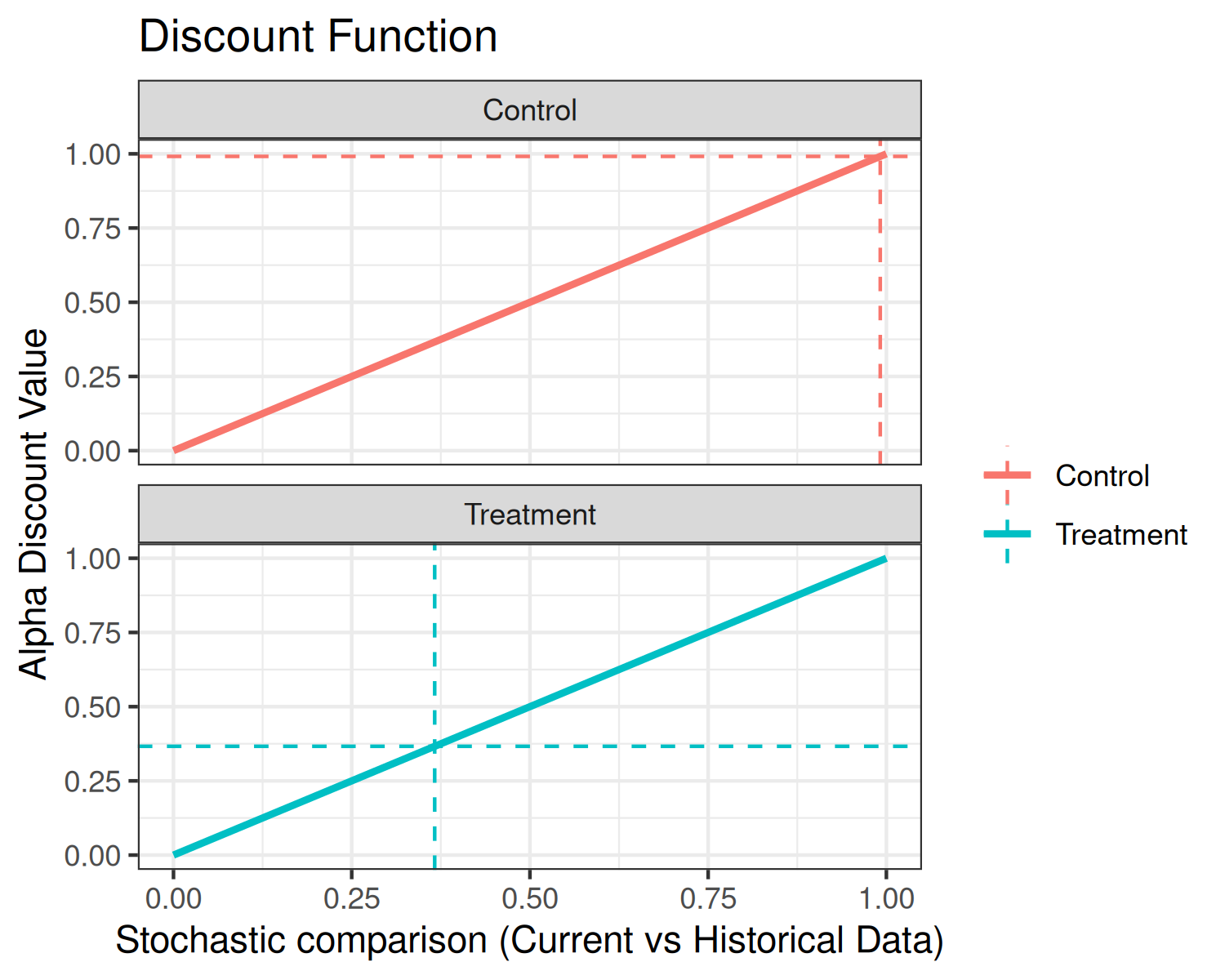

The bottom plot displays the discount function (solid curve) as well

as alpha (horizontal dashed line) and p_hat

(vertical dashed line). In the present example, the discount function is

the identity.

Two-arm trial

On to two-arm trials. In this package, we define a two-arm trial as

an analysis where a current and/or historical control arm is present.

Suppose we have the same treatment data as in the one-arm example, but

now we introduce control data: y_c = 15,

N_c = 200, y0_c = 20, and

N0_c = 250. This control data gives a current and

historical event rate of 20/250 = 0.08.

Before proceeding, it is worth pointing out that the discount function is applied separately to the treatment and control data. Now, let’s carry out the two-arm analysis using default inputs:

set.seed(42)

fit2 <- bdpbinomial(y_t = 15,

N_t = 200,

y0_t = 25,

N0_t = 250,

y_c = 20,

N_c = 250,

y0_c = 20,

N0_c = 250,

method = "fixed")

summary(fit2)##

## Two-armed bdp binomial

##

## Current treatment data: 15 and 200

## Current control data: 20 and 250

## Historical treatment data: 25 and 250

## Historical control data: 20 and 250

## Stochastic comparison (p_hat) - treatment (current vs. historical data): 0.3664

## Discount function value (alpha) - treatment: 0.3664

## Stochastic comparison (p_hat) - control (current vs. historical data): 0.9914

## Discount function value (alpha) - control: 0.9914

## alternative hypothesis: two.sided

## 95 percent CI:

## -0.0347 0.0453

## sample estimates:

## prop 1 prop2

## 0.08 0.08The summary method of a two-arm analysis is slightly

different than a one-arm analysis. First, we see p_hat and

alpha reported for the control data. In the present

analysis, the current and historical control data have event rates that

are very close, thus the historical control data is given full weight.

This implies that the (augmented) posterior control event rate is

approximately (20 + 20)/(250 + 250) = 0.08. Again, moderate

weight is given to the historical treatment data, so we have an

(augmented) posterior treatment event rate of 0.08.

The CI is computed at run time and is the interval estimate of the

difference between the posterior treatment and control event rates. With

a 95% CI of (-0.0347, 0.0453), we would conclude that the

treatment and control arms are not significantly different.

The plot method of a two-arm analysis is slightly

different than a one-arm analysis as well:

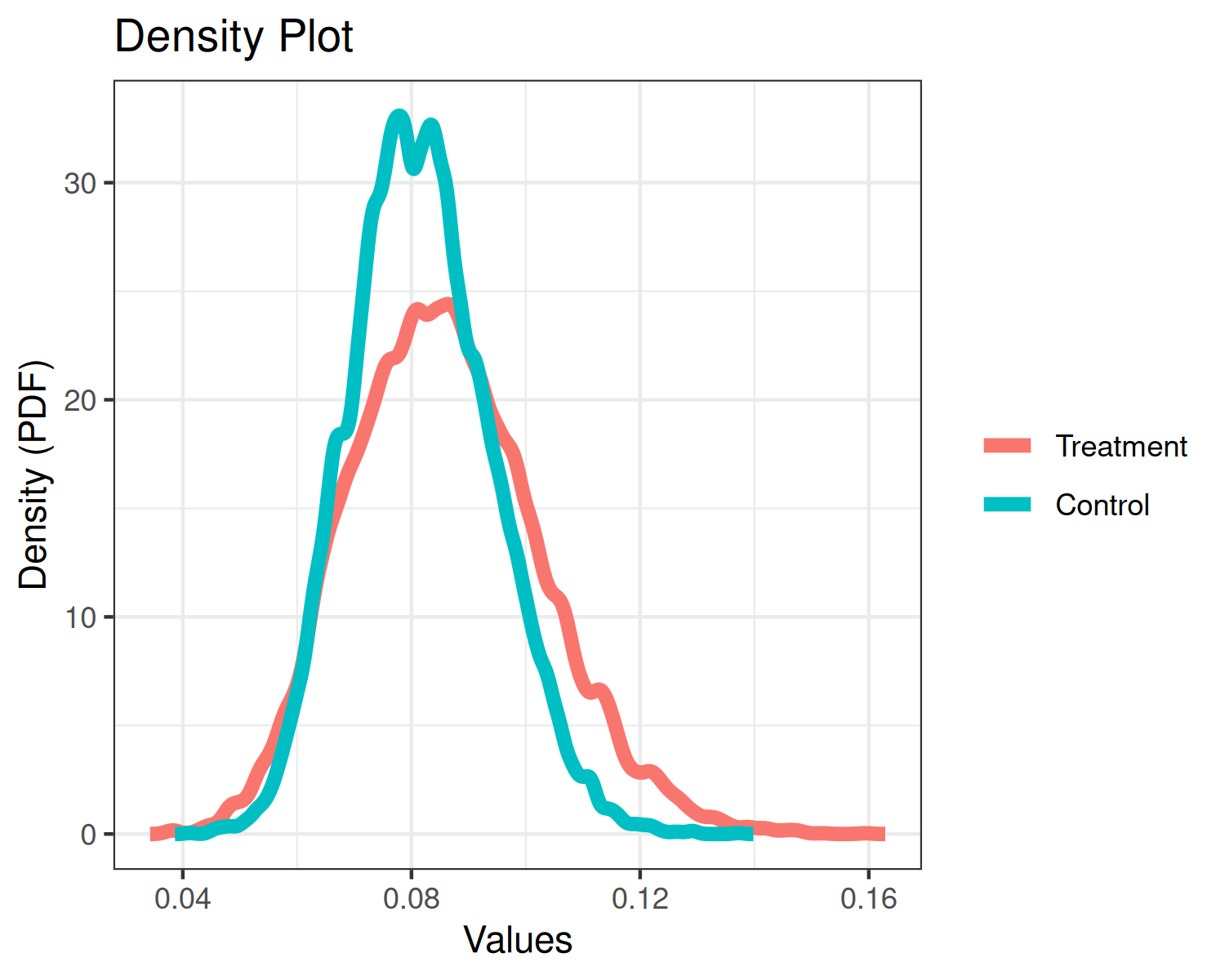

plot(fit2, type="posteriors")

plot(fit2, type="density")

plot(fit2, type="discount") Each of the three plots are analogous to the one-arm analysis, but each

plot now presents additional data related to the control arm.

Each of the three plots are analogous to the one-arm analysis, but each

plot now presents additional data related to the control arm.